In our last article with Meratas, we discussed how Income Share Agreements (ISA) loans are making education more attainable. So now that you have an idea of what an ISA is, how can you make sure that you’re getting one that works for you?

Educators work with platforms like Meratas to come up with unique ISAs that work for their needs. With many different payment structures and benefits, it can be hard to know which ISA is right for you without the right information to make an informed decision.

Meratas has worked with many schools and coding bootcamps over the years, and it’s learned a lot about what works and what doesn’t. Meratas uses this experience to help bootcamps and skills-training programs design student-friendly ISAs that work for both the schools and their students.

You can ask questions about the following features that Meratas suggests during your enrollment process to ensure you’re getting a fair and amazing ISA.

What Is an Income Share Agreement (ISA)?

As a reminder, an ISA is a type of loan that is a commitment between a funder (or a school) and a student. In an ISA, the funder (or school) covers the cost of the student’s education ventures, and the student agrees to pay back a percentage of their income after graduating and finding a qualifying job.

These are a few of the key terms that you’ll see in your ISA; income share percentage, the minimum income threshold, the payment window, required payments, and a payment cap.

Income Share Percentage

The Income Share Percentage (or ISP) is the percentage of your income that you will be obligated to pay to your school under your ISA. For example, if your income share percentage is 10%, and your gross monthly earnings are $4,000, then your monthly payments would be $400 (i.e., 10% of $4,000).

When considering ISA programs, be sure to ask your school if they offer an ISP discount for enrolling in autopay, which most schools do provide.

Minimum Income Threshold

Think of the Minimum Income Threshold as your “income floor.” With an ISA, Students don’t have to start paying back their ISA until they land a salary above their income floor (or minimum income threshold), and if your salary ever dips below your income floor, your payments automatically pause without accruing interest. This is one of the key benefits of having an ISA loan, and what makes them an attractive alternative to traditional private loans.

Payment Window

The payment window is the maximum length of time that your ISA contract is in effect. Since you only make ISA payments when earning above the income floor, your school will have a fixed amount of time to collect the agreement. We call this the “payment window.” With an ISA, once the payment window has elapsed, the ISA contract is terminated, regardless of the number of payments made. Even if you paid back less than the funded amount, your ISA still terminates at the end of your payment window.

Required Payments

The required payments are a set amount of payments that students know they’re required to make when they’re gainfully employed and earning above their income floor. Once a student has paid all of the required payments outlined in their ISA, the ISA is satisfied. A typical ISA may have 48 required payments, with a 96 month payment window. This payment window means that the school has 96 months to collect 48 required payments, but only if you are gainfully employed and earning above the income floor.

Payment Cap

Just like the minimum income threshold represents the “floor”, the payment cap represents the “ceiling”, or the most you might ever need to pay with an ISA. Since an ISA represents the student’s promise to share a portion of their income, this “ceiling” limits the amount of income a high-earner would ever need to share.

For high-earners, it is possible that you might hit your payment cap before you make all your required payments. In this case, the ISA terminates early even though not all required payments were made. When researching school programs, be sure to ask if they offer incremental payment caps, which lower your payoff amount if you pay faster than expected.

These ISA terms describe an important benefit of ISAs—the aligned risk and reward between students and their school. If students don’t land a job with a high enough salary within a certain amount of time after graduation, the school or funder won’t get paid. For this reason, ISAs align the incentives of school and student, ensuring that only those programs that produce real outcomes get financed.

Unlike traditional private loans, which fund the school in advance, with an ISA the school is incentivized to give its students the in-demand tools and training they need to get hired quickly at a good salary.

Even though you see these key terms in every ISA, there are a few features that go beyond this baseline. These student-friendly features set amazing ISAs apart, and add an extra layer of appeal to any ISA.

Student-Friendly Income Share Agreement Features

The best ISAs serve the needs of educators and their students. Meratas offers student-friendly technology to help schools build fair and easy agreements to please both sides of every agreement.

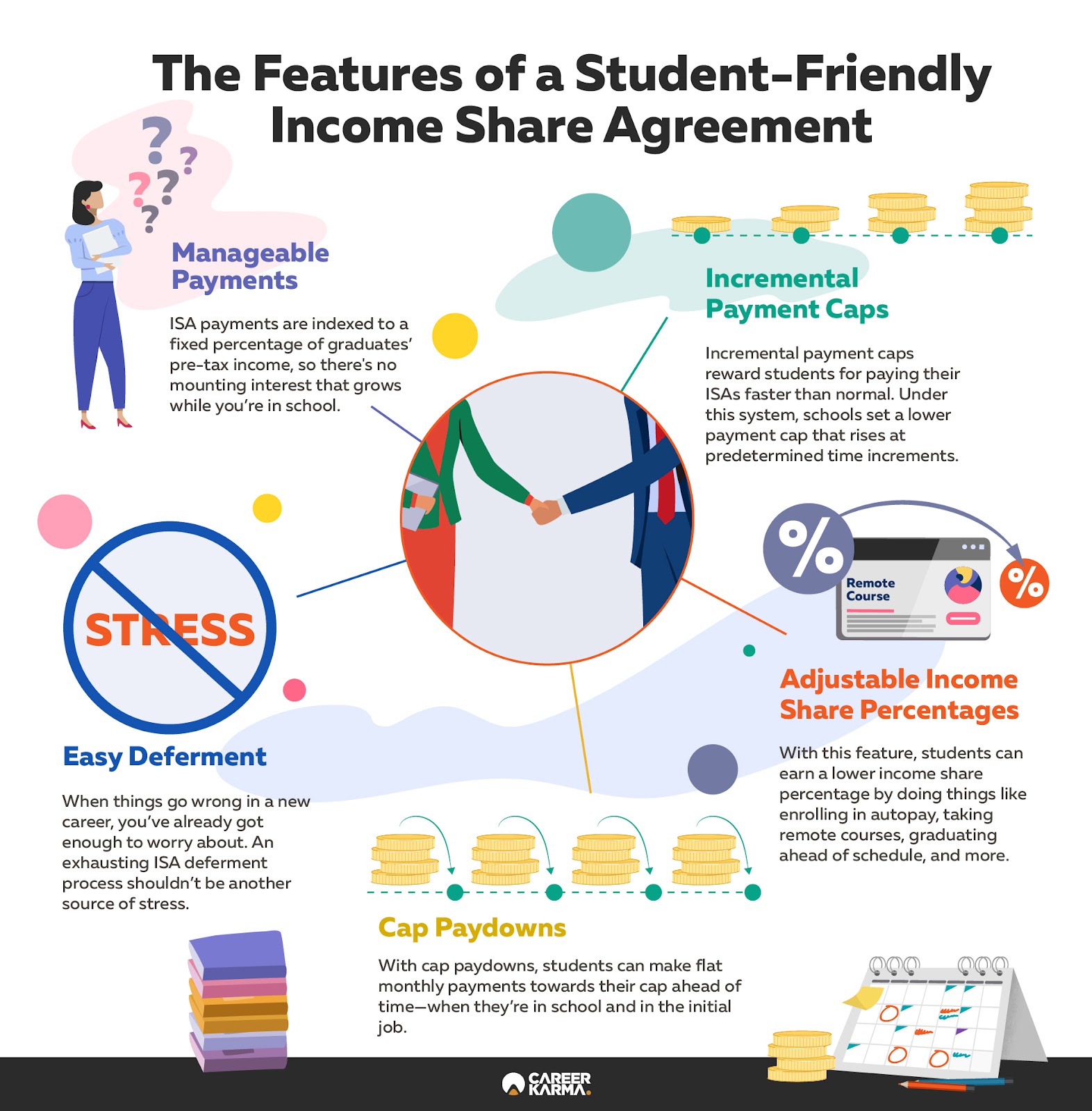

Meratas is the only ISA platform that offers certain additional features for stronger ISA contracts. These additional features include manageable payments, incremental payment caps, cap paydowns, and easy deferment. Though every Meratas ISA contract doesn’t contain these features, it’s the only ISA platform that makes these features available for its partners to build stronger student-focused agreements.

Manageable Payments

Manageable payments are the cornerstone of responsible ISA loan design. Schools, skills-training programs, and funders are all responsible for ensuring that graduates can afford payments based on expected outcomes in their new careers.

ISA debt payments are indexed to a fixed percentage of graduates’ pre-tax income instead of being tied to a principal sum and its interest. Because there is no principal like a traditional student loan, there is no mounting interest that grows while you’re in school or in deferment.

With a traditional private loan, even if you have deferment (or forbearance), the amount you owe is actually growing, due to interest accrual. This interest can leave students worse off than before, with ever mounting debt.

When designing an ISA program, schools usually ensure that payments will be manageable by looking at their program’s cost and the range of salaries that students can expect in the jobs associated with that program.

These facts mean that you’ll know roughly how much you should be paying once you land your qualifying job. ISAs have set finish lines and no surprises from the time you sign your contract to the time you submit your last payment. Because ISA recipients usually satisfy ISAs by making all of the required payments, you’ll know exactly how many times you’ll need to pay to satisfy your debt from the very beginning.

You can make sure your potential ISA has manageable payments by looking at the terms of the agreement along with expected salaries in the field in your area.

Let’s say, for example, you wanted to become a web developer in Nashville. The average salary for a web dev in Nashville is around $64,000 per year, according to Glassdoor. Because ISAs are indexed to your pre-tax income, your monthly salary would be about $5,333 for ISA purposes. So if you’re expected to pay 15% of that monthly salary back into your ISA, you’re looking at a very manageable $800 monthly payment.

Let’s say you’re required to make 32 payments in a 48-month window with a payment cap of $22,500 (1.5 times your tuition of $15,000), you’d be able to reach the payment cap and satisfy your ISA in only about 28 payments of $800.

But what if you were able to pay even less than the stipulated sum if you could commit to a bigger repayment every month?

Incremental Payment Caps: The Faster You Pay, The Less You Pay

Meratas suggests that schools add incremental payment caps to their ISA loans. Incremental payment caps reward students for paying their ISAs faster than normal. Under this system, schools set a lower payment cap that rises at predetermined time increments.

For example, a student signs up for an ISA with an incremental payment cap that rises by 10% every year. If they commit to paying more than the minimum each month, they can finish payments for just 10% more than tuition after finding a qualifying job. In the second year, the payment cap would rise to 20%, and in year three, 30%.

So the faster a student pays, the less they have to pay overall. This pay structure incentivizes students who can make higher payments to do so, with the added benefit of faster repayments. Incremental payment caps also work well for funders because they get a faster return on investment on the ISA.

Some ISAs also allow students to pay less just by taking certain actions that can help them in the long run.

Adjustable Income Share Percentages: Good Deeds Get Rewarded

Adjustable income share percentages give schools the freedom to reward students for doing things that help them.

With this feature, students can earn a lower income share percentage by doing things like enrolling in autopay, taking remote courses, graduating ahead of schedule, and more. By taking steps that help you build your career, you’ll have more money in your pocket as you start to find your footing.

Cap Paydowns: Pay More Now, Pay Less Later

Cap paydowns allow students to lower their ISA obligations while they’re still in their program.

With cap paydowns, students agree to make flat monthly payments during the time they’re in school and in the initial job search before they reach the minimum income threshold. These payments, which usually range from $200-$300 per month, end after students find a qualified job and switch to making regular ISA payments.

Schools can use cap paydown grants to reward students by either matching their payments or removing a flat amount from their total payment cap. Meratas’ partners commonly choose the second option. So if a student pays $200 per month during a seven-month job search, they’d have only paid $1,400 for the school to remove $5,000 or so from their payment cap.

This can be a good option for bootcamp graduates who have another source of income during their job search or are still not earning above the minimum income threshold. This option allows you to invest in yourself as you start a new career.

Easy Deferment: Quick and Painless

If you lose your job or dip below the minimum income threshold, it should be very simple for you to defer because of that job loss that you couldn’t control.

All ISAs automatically defer if your income dips below the threshold, but in cases of hardship, you may have to submit a deferment application. Meratas’ deferment application is a two-page document with simple yes or no questions. In its process, deferments are granted far more often than not.

If you’re still employed and making below the minimum income threshold, all you have to do is keep submitting your pay stubs and reporting monthly income to keep receiving deferment. If you’ve lost your job, Meratas asks for a date of termination and a letter of termination. Any student that complies with this process will receive deferment as long as they’re under the minimum income threshold.

Students just have to make sure that Meratas knows they’re still unemployed or under the income threshold each month to continue receiving deferment on their payments.

When things go wrong in a new career, you’ve already got enough to worry about. An exhausting ISA deferment process shouldn’t be another source of stress.

Conclusion

These Meratas-exclusive student-friendly features can make career changes easier for both you and the ISA provider. But it’s important to remember that even if a school’s ISA doesn’t contain these features, it can still be a great financing option.

Be sure to go over the numbers on any possible ISA to determine if it’s a good option if it doesn’t include the student-friendly features we’ve discussed above. At the very least, any good ISA should have a fair minimum income threshold, monthly payment amount, and amount of required payments based on the expected career outcome.

These benefits are just an added foundation for discussing ISAs with your school or skills-training program’s financing office. Use your best judgment about which of these features would work best for you, and which you may not necessarily need for a quality experience.

If you’d like to learn more about the ways that Meratas works with programs to build great ISAs that benefit their students, feel free to visit its Student Guide.

About us: Career Karma is a platform designed to help job seekers find, research, and connect with job training programs to advance their careers. Learn about the CK publication.